Life cycle programs for powder and bulk processing plants

Bob Mcilvaine is the president of the Mcilvaine Company in Northfield, Illinois. Mcilvaine provides market research and technical analyses on powder and bulk solids handling equipment. He may be reached at [email protected] or 847-784-0012, ext. 112. Mcilvaine is a regular columnist in Processing. This column appeared in the March 2019 issue.

The Industrial Internet of Things (IIoT) empowered by the Industrial Internet of Wisdom (IIoW) is changing the powder and bulk solids industry. With remote monitoring and data analytics, the cost of a component and its replacements can be accurately determined over time. This opens the door for suppliers that can offer life cycle programs with lowest total cost of ownership (TCO). The concept applies to small operations as well as large ones.1

A big chemical company can easily justify automation, centralized purchasing and TCO determinations. It can compare the performance of hundreds of blowers throughout its many plants, for example. The time spent on lowest total cost of ownership validation (LTCOV) can be apportioned over many purchases and easily justify the cost.

Small plants, however, are now finding that life cycle cost management programs are more affordable due to the decreasing cost of wireless transmission and process management software. Hot mix asphalt plants are a good example. There are more than 3,000 hot mix asphalt plants in operation in the U.S. Even with a crew of four or more operators it has become a challenge to deal with variations in sand moisture as well as changing percentages of recycled asphalt pavement and shingles in the mix. Thanks to automation and as many as 20 video cameras at a given site, the proportions in the mix can be remotely optimized. Component performance can then be analyzed and repairs made as necessary. The operating crew can be reduced to one or two people.

The number and stringency of government regulations keeps increasing, especially in the food and pharmaceutical industries, such as new regulations to protect workers from silica dust. Tougher safety restrictions starting in 2020 will aim to protect against explosions in the food, grain and other powder processing industries. Due to the changing regulations, review and compliance should be viewed as a continuing life cycle requirement.

Larger companies can provide life cycle programs due to the number of divisions and breadth of product offerings. This is a challenge for smaller companies. However, one company meeting this challenge is IAC, an industrial equipment and procurement contractor (EPC) that designs large systems for a number of manufactured sand plants as well as for clients in aggregate, cement and steel. The company recognizes the advantage of offering a range of services that span the life of the plant. These services can be summarized as Advise-Design-Supply-Construct-Guide-Maintain.

IAC is applying this life cycle support program to the manufactured frac sand industry, which is rapidly growing and evolving.

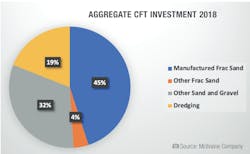

The importance of the manufactured frac sand on the U.S. powder and bulk solids market is shown in Figure 1 (above). The number of tons of manufactured frac sand is small but the CFT expense per ton is high. Also, the growth rate will be much higher than other granular categories. As a result, most of the revenue growth in 2019 will be in manufactured sands (see Figure 2).

Source: The Mcilvaine Company

The total production of frac sands in the U.S. will exceed 100 million tons this year at an average selling price of more than $60 per ton, creating a $6 billion market. The revenues for powder and bulk handling suppliers are much higher per ton of product because much of the production is shifting to local manufactured sands. This means the big cost is in the processing and not the freight.

This fundamental shift in U.S. frac sand production is away from the Midwest, home to the highest quality Northern White, to lesser-grade sands, which are then upgraded (manufactured). As a result, Northern White’s market share is expected to be 43 percent in 2019, down from 75 percent in 2014.

Various granular products require dry or wet processes. Some require both. These involve some combination of pneumatic or mechanical conveyors, pumps, valves, scrubbers, fabric filters, precipitators, filter presses, centrifuges, dryers, classifiers, fans, controls and instrumentation.

According to the United States Geological Society’s (USGS) Mineral Resource Program, in 2017, 890 million tons of construction sand and gravel valued at more than $7.7 billion was produced by an estimated 3,600 companies operating 9,400 pits and 360 sales/distribution yards in 50 states. Leading producing states were, in order of decreasing tonnage, California, Texas, Minnesota, Michigan, Arizona, Colorado, Washington, Ohio, Wisconsin and New York, which together accounted for about 52 percent of total output. It is estimated that about 44 percent of construction sand and gravel was used as concrete aggregates; 25 percent for road base and coverings and road stabilization; 13 percent as asphaltic concrete aggregates and other bituminous mixtures; 12 percent as construction fill; 1 percent each for concrete products; and the remaining 3 percent for filtration, golf courses, railroad ballast, roofing granules and other miscellaneous uses.

Whether it is sand, gravel, grain, manufactured frac sands, chemicals or pharmaceuticals, customers will be looking for suppliers that offer life cycle programs for powder and bulk processing.

References

1. IIoT and Remote Monitoring, published by the McIlvaine Company