How to modernize tank and terminal systems for accurate accounting

In modern tank and terminal facilities, material transfer operations include a mix of legacy processing systems still in use, new technologies installed to improve operations and tank monitoring software. But some older facilities have not modernized their operations, and can be losing millions of dollars in unaccounted losses, especially if they are dispensing more materials to customers than they are getting paid for. Conversely, errors can be made in the other direction, shortchanging and overcharging customers, leading to loss of business and other issues.

Oil and gas companies are familiar with the accuracy standards imposed by custody transfer regulations, but older chemical plants may still be working with legacy control systems and outdated instrumentation that can’t provide the necessary accuracy for accounting purposes.

Updating and modernizing tank and terminal systems requires a complete analysis of the measuring instrumentation, the methods used to convert measurements to volume, and the accuracy of all the techniques involved. An assessment of the current situation is the best place to begin the process of “accounting for the unaccounted.” The first place to start is to evaluate the measuring of the product, whether it is an inbound or outbound transaction.

The measurement

Users first need to assess the accuracy of the measurement instrument itself to determine if it meets requirements. A quick example: To loadout 5,000 gallons of a product, how accurate should a measurement instrument be to ensure that the customer is getting 5,000 gallons? Will the accuracy need to be within ½ gallon, 1 gallon or 20 gallons?

If the transaction will only happen twice a week with a ±20-gallon accurate instrument, the unaccounted loss could be as high as 40 gallons. If this transaction occurs 1,000 times a week, there could be an unaccounted loss of up to 40,000 gallons. If the product sells for $2.50 per gallon, then financially an unaccounted loss of up to $100,000 per week will be possible. On the other hand, if a ±½ gallon accurate instrument is chosen, then the unaccounted loss can be reduced to 500 gallons, saving up to $98,745.

The frequency, quantity and cost of product are the criteria determining the instrument accuracy that should be deployed to measure the transfer. Whether this is a flow, volumetric or weight measurement, the accuracy of the instrument will have a significant financial impact.

In most legacy control processes, the instruments were selected long ago to provide measurement data to the control system. They were usually not chosen based on the financial impact the measurements could have on the profits and reputation. But this situation can be corrected by using instruments which fulfill both roles, providing both precise control of operations and accurate financial accounting.

Accuracy of unit conversion

Consider a tank or storage vessel being filled or loaded with product. It has a capacity of 30,000 gallons, and the operational control indicates the operator should stop filling when the vessel gets to 85 percent of capacity. The process engineer indicated that an accuracy of 2 percent was acceptable for control purposes, and if the tank reached 87 percent it still would not pose an overspill risk. So, with a 2 percent accurate instrument and the control mechanism programmed to stop at 85 percent, an unaccountable loss of up to 600 gallons could occur.

In this example, the process data generated is in unit percentage. This is great for filling and emptying the vessel, but financially it is the wrong unit of measure. The right unit would be the actual number of gallons in the vessel, which might require an entirely different measurement system.

Using unit percentage, the measurement device must be configured to the appropriate sensing range, and this range must be scaled to indicate 0 to 100 percent. This type of measurement system is difficult to set up to a high degree of accuracy, and difficult to maintain, as will be shown in the subsequent sections.

Measurement to signal

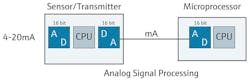

The next conversion to consider takes place from the measurement instrument to the control system. The control system is almost always a form of microprocessor-based device, so the analog instrument data must be converted to a digital signal.

First, the measurement data in the instrument in digital form will get converted in a digital-to-analog (D/A) converter, and then represented as a 4-20 mA signal (see Figure 1). This 4-20 mA signal will then go to an analog input converter on the control system’s microprocessor where the conversion process is reversed, with the resulting digital value placed into a memory register in the microprocessor.

Most legacy microprocessor systems employ a 16-bit A/D conversion in the system’s architecture, so the 4-20 mA signal is now represented in memory as an integer value of 3277-16384, or 13,107 digital units of accuracy. It is now up to a control systems engineer to convert this digital value stored in memory to a 0 to 100 percent reading.

Considerations in this process of signal conversion include making sure the instrument range, the D/A conversion resolution of the signal transmitter, and the A/D conversion resolution in the microprocessor have enough units of accuracy.

In the example, the system is not taking advantage of all the resolution available. The process data of 100 percent provides only 100 units of accuracy, while the control system is capable of 13,107 units of accuracy; hence 1,310 units of accuracy are wasted.

In this case, the control system can accept an input from a measurement device that is accurate to thousandths of a percent. In theory, the potential unaccounted volume could be reduced from 600 gallons to 0.6 gallons, or 599.4 gallons. If the cost of the product is $2.50 per gallon, then unaccounted losses can be reduced to $1,498.

Removing the analog signal conversion helps eliminate most signal conversions. This can be done by replacing each level measurement instrument with one that can transmit the measurement as a digital value by using EtherNet/IP or another Fieldbus network and protocol (see Image 1).

Conversion to volume

Assume the measurement data is in the control system as a percentage; that is sufficient for operations, but not for accounting. How can this unit percentage data now be manipulated and converted?

Continuing to use a 30,000-gallon vessel as an example, the control system can convert percentage into gallons. The data can simply be linearized; i.e., 0 to 100 percent times 30,000 gallons. If the vessel is a standard geometrical shape, this will work. However, if it is not (and this is most likely the case), then an equation needs to be generated, with some vessels requiring complex algorithms.

The process of “volume conversion” needs to be scrutinized to determine if accuracy can be improved. The first consideration is the physical measurement to physical volume data resolution. Whichever physical measurement is employed, it must be reconciled to actual physical volume using a lookup table. The more physical data points referenced, the more accurate the volume conversion is. In some cases, only two data points are employed – empty and full – with everything between these two points an approximated value, clearly not suitable for accounting purposes.

The next consideration is understanding the transfer process and its impact on the physical properties of the material. The transfer process into storage vessels creates waves, which can artificially increase the measurement reading. These waves can also introduce air into the material, and the agitation from the process can create foaming of the product.

All these factors need to be considered to determine when and where the measurement should take place to yield the most accurate reading. For example, will settling times need to be introduced to reduce the effect of mechanical waves, or to allow foaming to subside? Will locating the instrument in a different position yield more accurate measurements? Will the type of level instrument need to be changed?

The next consideration when converting to volume is the effect temperature can have on the storage vessel and the product in the vessel. Some materials will expand and contract when temperatures rise and fall. To achieve higher accuracies of measurement, temperature compensation can be employed to account for this expansion and contraction. In some cases, it is useful to insulate vessels to reduce the required volume correction.

Another consideration is the pressure the product exerts on the mechanical structure and shape of the vessel. If the mechanical structure flexes while holding the product, then volume correction may need to be factored to account for this condition.

When an accurate volume measurement has been achieved by taking all these factors into account, a conversion from volume to mass typically needs to occur because most transactions are based on weight.

A simple upgrade for a process needing accurate mass or volume measurements is to install a flow instrument that can calculate these values automatically (see Image 2). This eliminates the need to perform manual or computer-based calculations.

Volume to mass

Conversion from volume to mass can be simple and straightforward, but not always. Once the density of a product is known, volume multiplied by density will yield the mass of the product. The next step is to multiply by a weight correction factor – typically calculated by taking into account the effect of gravity at atmospheric conditions and adjusting for any impact that pressure can have on the measured product – to determine weight.

However, as usual there are some considerations that need to be addressed; first is the temperature effect. Does the density of the product change as the temperature of the product changes? If so, then referencing a density lookup table will help improve the accuracy of the conversion and final measurement. And are there other substances in the material such as sediment or water that should not be part of the calculated weight? If so, these substances must be accounted for.

Another solution for both volume and mass measurements is to use specialty tank inventory control hardware and software (see Image 3) to perform the required complex tank and vessel calculations.

Summary

To reduce unaccounted lost revenue in the inventories and transfers of products, or to avoid overcharging customers, several considerations need to be reviewed, understood and possibly improved upon:

- The accuracy of the measurement instrument

- The signal conversion process

- Unit conversion to volume

- Unit conversion to mass, weight and currency

An assessment can be made once these steps have been evaluated and the considerations of frequency of transactions, quantity of transaction, and cost of product are applied. This assessment will reveal where upgrades should be made to improve operations and produce a more accurate accounting.

Michael Robinson is national marketing manager for Projects, Services and Solutions for Endress+Hauser in the United States. Robinson has served the industrial automation market since 1994 when he began work as a controls engineer for an OEM equipment manufacturer in Southern California after graduating from Cal Poly San Luis Obispo.