Markets Update: Global flowmeter market to approach $9B by 2023

Global flowmeter market to approach $8.85B by 2023 led by Coriolis and ultrasonic

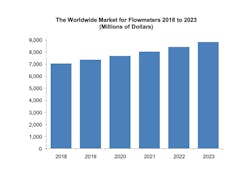

A new study from Flow Research finds that the worldwide flowmeter market totaled $7.06 billion in 2018 and is projected to approach $8.85 billion by 2023.

The worldwide flowmeter market size has followed the upward and downward fluctuations in oil prices. When oil prices began dropping five years ago and many oil and gas exploration projects were postponed or canceled, associated instrumentation industries experienced a ripple effect. This downturn especially impacted the Coriolis, ultrasonic, differential pressure, positive displacement and turbine flowmeter markets.

In 2015, for the first time in many years, new technology flowmeter markets showed a decline. The only exception was a small revenue increase for magnetic flowmeters, which cannot measure the flow of hydrocarbons and therefore are not widely used in the oil and gas industry.

Fortunately, in February 2016, oil prices began recovering and the worldwide flowmeter market is now back on a healthy upward track. Coriolis and ultrasonic flowmeters, which are industry-approved for custody transfer of both gas and liquids, are projected to experience the fastest growth rates over the next four years.

While new technology flowmeters are displacing traditional technology meters in some applications, it is clear that traditional meters are still a major force in the flowmeter market. New technology flowmeters – meters first introduced after 1950 – include Coriolis, magnetic, ultrasonic, vortex and thermal flowmeters. Traditional technology flowmeters include differential pressure (DP), positive displacement, turbine, open channel and variable area flowmeters.

Image courtesy of Flow Research

Industrial pumps market worth $90B by 2026

According to Acumen Research and Consulting, the global industrial pumps market will reach around $90 billion by 2026 and is expected to grow at a compound annual growth rate (CAGR) around 6% between 2019 and 2026.

Growing use of industrial pumps in various applications including wastewater treatment and chemicals is likely to drive the market over the forecast period. Demand for industrial pumps from process and manufacturing industries is another driving factor of the market. The rise in product energy pumps for the transportation and extraction of oil and natural gas is having a positive effect on the market. Increase in crude oil price is also boosting the demand for the market as it fuels the energy sector’s revenue.

Growing construction, automotive and manufacturing industries are expected to raise the demand for industrial pumps in Asia-Pacific regions. The Indian government has passed a policy for the promotion of FDI investment in the oil and gas sector. This will increase the production of petrochemicals and polymers in the country, hence propelling the demand in this region. Increased investment in desalination plants is also expected to increase the sale of industrial pumps.

Further key findings from the report suggest:

- Centrifugal pumps hold a major share of the market and are segmented into multistage pump, single-stage pump, submersible pump, sealless and circular pump, and axial and mixed flow pump.

- Centrifugal pumps will dominate the market for industrial pumps. These pumps can handle varied pressure and have good load handling capabilities with comparatively low maintenance cost.

Key trends in the industry:

- Growth in process manufacturing activity will result in an increase in demand for positive displacement pumps.

- Positive displacement pumps held a market share of 13% in the year 2018 and are forecasted to generate revenue of $10.71 billion in the year 2026 with an annual growth rate of 5.3% throughout the forecast period.

- With an increase in manufacturing activity, demand for aftermarket parts will benefit, majorly for the chemical industry as they have harsh environments.

- Increase in infrastructure sector in Asia-Pacific countries like India, China and Japan are boosting the market of industrial pumps. The emergence of manufacturing industries and automotive is also propelling the demand in this region.

Global dust extractor sales set to grow 6% year-over-year

Global sales of dust extractors exceeded the revenues worth $1 billion in 2018, and they are projected to experience a year-over-year growth of around 6%, in 2019 and ahead. According to research from Future Market Insights (FMI), dust extractors will see significant gains in the low dust class, accounting for a substantial incremental opportunity over the coming years.

While adoption of dust extractors in medium dust class will retain a dominant share over that in the low dust class in the long run, the latter is highly likely to outpace the former owing to the impressive growth of commercial building sector. Sales are likely to experience a considerable hike in the forthcoming years, as the demand from major end-use sectors, particularly commercial building and offices, is on a constant rise.

Construction sites, though expected to remain the key demand generator in the dust extractor space, will be closely trailed by the wood working segment. The report positions wood working applications of dust extractors market as an important demand contributor to the market and projects a healthy rate of growth for the dust extractor demand in wood working segment.

Integrated cybersecurity and service-based business models help vendors expand customer base, finds Frost & Sullivan

As end-user industries embrace the concept of Industrial Internet of Things (IIoT) or Industry 4.0, there will be greater demand for IT-operational technology (OT) convergence. In this environment, distributed control system (DCS) vendors that are keen to prove their agility and adaptability will look to innovate in the software segment to create value for end users. The revenue opportunities in evolving into an open, secure and interoperable DCS system is expected to drive the $14.79 billion DCS market toward $17.14 billion by 2025, according to research from Frost & Sullivan.

"Owing to the higher adoption of digitalization in end-user industries, DCS vendors are collaborating with IT providers to develop digital capabilities. Startups with niche capabilities will, therefore, play a crucial role in the future of industrial automation," said Rohit Karthikeyan, senior research analyst for Frost & Sullivan’s global industrial team. "Meanwhile, as end users’ projects increase in scale and complexity, their dependence on main automation contractor (MAC) will also rise. Consequently, DCS vendors will strive to develop MAC capabilities to execute end-user automation projects and gain a competitive advantage.”

Karthikeyan noted that going forward, the growth in emerging Asian countries will expand APAC’s share of the global DCS market revenues to 34.8% by 2025 . "Investments in new pipeline projects from the Middle East to Central Europe and refinery projects in countries such as Germany, France and Italy are expected to lead to new midstream and downstream project activities and ultimately, revenue opportunities in the next three to five years," Karthikeyan said.